IMF Managing Director Kristalina Georgieva has warned the coronavirus pandemic will turn global economic growth “sharply negative” this year.

She said the world faced the worst economic crisis since the Great Depression of the 1930s.

The head of the International Monetary Fund forecast that 2021 would only see a partial recovery.

Lockdowns imposed by governments have forced many companies to close and lay off staff.

Earlier this week, a UN study said 81% of the world’s workforce of 3.3 billion people had had their place of work fully or partly closed because of the outbreak.

Kristalina Georgieva made her bleak assessment in remarks ahead of next week’s IMF and World Bank Spring Meetings.

Emerging markets and developing countries would be the hardest hit, the IMF chief said, requiring hundreds of billions of dollars in foreign aid.

She said: “Just three months ago, we expected positive per capita income growth in over 160 of our member countries in 2020.

“Today, that number has been turned on its head: we now project that over 170 countries will experience negative per capita income growth this year.”

Kristalina Georgieva added: “In fact, we anticipate the worst economic fallout since the Great Depression.”

She said that if the pandemic eased in the second half of 2020, the IMF expected to see a partial recovery next year. But she cautioned that the situation could also worsen.

Kristalina Georgieva’s comments came as the US reported that the number of Americans seeking unemployment benefits had surged for the third week by 6.6 million, bringing the total over that period to more than 16 million Americans.

On April 9, following marathon talks, EU leaders agreed a €500 billion ($546 billion) economic support package for members of the bloc hit hardest by the lockdown measures.

The European Commission earlier said it aimed to co-ordinate a possible “roadmap” to move away from the restrictive measures.

Earlier this week, the International Labor Organization (ILO), a UN agency, warned that the pandemic posed “the most severe crisis” since World War Two.

The ILO said the outbreak was expected to wipe out 6.7% of working hours across the world during the second quarter of 2020 – the equivalent of 195 million full-time workers losing their jobs.

Last month, the Organization for Economic Co-operation and Development (OECD) warned that the global economy would take years to recover.

OECD secretary general Angel Gurría said that economies were suffering a bigger shock than after the 9/11 terror attacks of 2001 or the 2008 financial crisis.

The harsh reality of the modern job market is that few

professionals stay at one company or in one position for more than a few years

at a time. This obviously presents enormous opportunities for pros to follow

various career paths. But at the same time, finding yourself in between jobs

can be quite unsettling for some. Those used to a regular nine-to-five workday

might even be overwhelmed by the amount of free time unemployment entails. With

that in mind, today we’re going to share five tips that professionals can use

to stay sharp in between jobs. Check them out here:

Take Job-Hunting

Seriously

It can be very tempting to blast out hundreds –– or even thousands –– of resumes at one time. While this approach may produce results for some, the fact of the matter is that it’s much better to tailor your resume and cover letter to specific jobs you find. Not only do you have a better chance of landing an interview with this approach, but it also allows you to get to know a prospective employer and decide if their company a good fit for you. Remember, taking the first job you’re offered isn’t always the best way to go.

Learn Something New

Every Day

Each day presents a chance to improve yourself and gain more knowledge. As such, make it a point to use your free time productively. Spend an hour at the library, sign up for a dance class, volunteer at a local charity –– just make sure to do something worthwhile that exposes you to new experiences.

Pick up a Side Hustle

Just because you’re in between jobs, it doesn’t mean the bills will stop coming. Thankfully, getting a part-time job can help you keep the creditors at bay. In addition to trendy side hustles like Uber, Lyft, and Airbnb, you should also consider freelancing in your field. Writing blogs or designing web pages is a great way to bolster your C.V. when you don’t have a full-time position.

Study How the Best Work

If you want to become a better chef, then it makes sense to watch videos on how professionals like Gordon Ramsey cook. In the same vein, if your goal is to open up a small business, then it’s a good idea to peruse successful small business websites, like this one from OTW Safety, for instance. What’s more, speaking to leading minds in your industry can grant you valuable insights that you can use to further your own career.

Stay Positive

Sometimes it takes a while to find a job on the market. The key

is to not get discouraged. Staying positive might be difficult, but it will

enable you to reach your goals in the long run.

The US economy added 292,000 jobs in December 2015, beating expectations, the Bureau of Labor Statistics data shows.

The data also showed the jobless rate held at its seven-and-a-half year low of 5%.

Professional and business services, construction, health care, and food services all saw job increases.

As well as the strong December jobs figures, US employment figures for October and November 2015 were revised up sharply to show 50,000 more jobs created than previously reported.

The robust figures come after the first US interest rate rise in nearly 10 years in December 2015.

The Federal Reserve raised overnight interest rates last month by a quarter of a percent to between 0.25% and 0.50%.

Construction and mining equipment maker Caterpillar has announced it could cut its workforce by more than 10,000 by 2018.

The US-based company – which employs more than 126,000 worldwide – said it would cut up to 5,000 jobs by the end of 2016.

Caterpillar is looking to reduce annual costs by $1.5 billion by the end of 2016.

The company has been hit by the collapse of commodity prices which have affected its key customers in the mining and energy sectors.

It has reduced its revenue forecast for this year by 2% to $48 billion and says 2016 earnings will fall 5%.

It will be first time in Caterpillar’s 90 year history that sales revenues have fallen for four years in a row.

Caterpillar shares were the biggest faller on the Dow Jones index on September 24, losing almost 6% as the market opened.

Doug Oberhelman, Caterpillar chairman and chief executive, said: “We are facing a convergence of challenging marketplace conditions in key regions and industry sectors – namely in mining and energy.”

The company has reduced its total workforce by more than 31,000 since mid-2012.

Caterpillar warned there could be a “total possible workforce reduction of more than 10,000 people” and said it expected to close some 20 manufacturing facilities over the next three years.

Doug Oberhelman said: “While we’ve already made substantial adjustments as these market conditions have emerged, we are taking even more decisive actions now.

“We don’t make these decisions lightly, but I’m confident these additional steps will better position Caterpillar to deliver solid results when demand improves.”

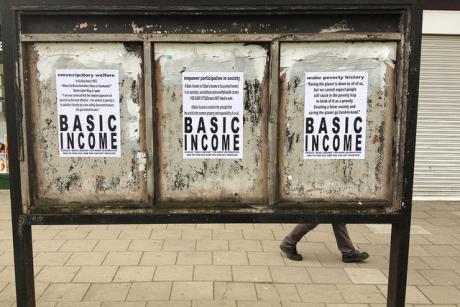

Finland is planning to start a pilot project that would see the state pay people a basic income regardless of whether they work.

The details of how much the basic income might be and who would be eligible for it are yet to be announced, but already there is widespread interest in how it might work.

Finland’s PM Juha Sipila has praised the idea.

“For me, a basic income means simplifying the social security system,” he said.

The scheme is of particular interest to people without jobs. In Finland, they now number 280,000 – 10% of the workforce.

With unemployment an increasing concern, four out of five Finns now are in favor of a basic income.

In Finland, taking on work can cost you money if you are unemployed.

A paid temporary job means lower welfare benefits.

If that job comes from a low-wage sector, you lose out because there is a delay before the authorities allow your benefits to be restored once you have left the job.

Many Finns nowadays have what are described as atypical working lives, in that few spend their entire lives in the same occupation and with the same employer.

This fundamental change has prompted a need for reforms to the social security system.

Supporters of the basic income believe it could offer an alternative to Finland’s complex and costly benefit models.

The prime minister has expressed support for a limited, geographical experiment. Participants would be selected from a variety of residential areas.

One obstacle to staging a pilot project is Finland’s constitution, which states that every citizen must be equal.

Even a small-scale experiment would put its participants in an unequal position.

Greece’s unemployment rate reached a record high of 28% in November 2013, according to newly released government figures.

The jobless rate increased from 27.7% in the previous month. For those under the age of 25, unemployment hit 61.4%.

Harsh austerity measures have led the Greek economy to shrink by a quarter in four years.

However, other economic indicators have suggested that there are signs of recovery.

Before Greece received its first 110 billion-euro ($150 billion) bailout in May 2010, the jobless rate was under 12% here.

Slight growth is expected this year and the deficit now wiped out, apart from interest payments on the bailout.

Greece’s unemployment rate reached a record high of 28 percent in November 2013

Greek unemployment is more than twice the average rate in the eurozone.

According to official EU figures, the number of people out of work in the single currency bloc in December was 19 million, with the jobless rate at 12%.

Other economic figures such as retail sales, manufacturing activity and construction, have pointed to signs that Greece’s recession has bottomed out.

However, Greece’s unemployment rate is expected to rise further in the first three months of 2014 as firms continue to restructure and cut jobs.

With 1.38 million people officially jobless, turning around the country’s economy will take time, even if the recovery does start this year as Athens hopes.

Before the crash when Greece was growing at up to 5% annually, about 50,000 jobs a year were added to the economy.

At these rates it could take more than 20 years to reduce the jobless totals – without measures to encourage domestic and foreign investment.

According to official figures, the US economy added 113,000 jobs in January, weaker than expected for a second consecutive month.

Economists had predicted an increase of about 180,000 new jobs last month.

However, the unemployment rate fell to 6.6%, the lowest level since October 2008, as more people began looking for work.

The US economy added 113,000 jobs in January, weaker than expected for a second consecutive month

The jobless figures will raise concern that, after a strong second half of 2013, growth in the US economy is beginning to lose its steam.

Earlier this week an unexpectedly weak manufacturing report raised concerns about the strength of the US economy and sent the Dow Jones tumbling by 326 points.

December’s surprisingly weak figure was revised up only modestly to 75,000, from 74,000.

The construction industry, most vulnerable to the impact of bad weather, added 48,000 in January indicating that while the weather may been responsible for December’s weak figures, it does not appear to have been a factor in January.

The US jobless rate fell to a five-year low of 6.7% in December as companies created 74,000 new jobs, latest figures show.

However, the number of jobs created was the lowest for three years and was well under half the number expected by analysts.

The US had bad weather in December, which may have stalled hiring plans.

The fall in the rate, now at its lowest since October 2008, in part reflects people leaving the labor force.

The government counts people as unemployed only if they say they are actively searching for work.

The US jobless rate fell to a five-year low in December 2013

The leisure, manufacturing and services sectors added jobs in December, but construction cut 16,000 jobs, the biggest drop in the industry in 20 months.

In the four months before December, the average number of jobs created in the US was 214,000 a month.

Other figures on employment have suggested a healthy jobs market, and the Labor Department said 38,000 more jobs in November were created than the 203,000 previously reported.

Overall, the US economy is picking up steam, with recent figures for consumer spending, trade and factory output all strong.

This year, economists expect the US economy to grow by 3%, well up on the 1.7% last year.

The improving picture led the Federal Reserve to start to taper its massive monetary stimulus program from $85 billion a month to $75 billion.

If the Fed remains confident about the direction of the economy, it may trim this back further at its next meeting at the end of this month.

The meeting will be the last one chaired by Ben Bernanke, who will leave the post after eight years. He will be replaced by Janet Yellen on February 1st.

The US Labor Department has announced the unemployment rate fell to a five-year low of 7% in November.

Payroll figures also showed that 203,000 jobs were created last month, more than predicted, as the US economy displayed more signs of strength.

The monthly non-farm payroll figure is watched closely by economists.

Analysts say these indications of strong growth could mean that the Federal Reserve will start to unwind its massive stimulus programme soon.

However, the November figure might have been distorted. Some federal workers who were counted as jobless in the October – because of the 16-day partial government shutdown – returned to their jobs last month.

The latest data also showed that the October and September non-farm payroll figures, which had also been strong, were even better than their first estimates.

The US unemployment rate fell to a five-year low in November

Job gains for those two months were revised upwards by 8,000.

Chris Williamson, chief economist at research firm Markit, said the data indicated the US labor market was “buoyant”.

“The decline pushes the jobless rate down to its lowest since November 2008 and closer towards the Fed’s threshold of 6.5%, which it wants to see breached before it considers tightening policy via higher interest rates,” he said.

But he added that a decision on when the Fed might start to taper its stimulus programme was still not clear cut.

The labor market figures follow news earlier this week that economic growth, as measured by GDP, in the third quarter of the year was revised up to an annual pace of 3.6% from a previous estimate of 2.8%.

Also on Friday, the US Commerce Department said that consumer spending increased in October, though wages and salaries were barely changed.

According to the latest figures from the Labor Department, the US economy added a better-than-expected 204,000 jobs in October.

There had been fears that the 16-day shutdown of government services last month could have hit jobs growth.

The monthly non-farm payroll figure is taken as a key indicator of the health of the world’s biggest economy.

However, the latest figures also showed that the unemployment rate edged up to 7.3% from 7.2% in September.

The Labor Department said that this was likely to be because many federal workers were counted as unemployed during the shutdown.

The report also said that employers added 60,000 more jobs in September and August than earlier estimates had suggested.

The US economy added a better-than-expected 204,000 jobs in October 2013

The latest figures add to a positive week for US economic data.

On Thursday, it was announced that the US economy grew at a better-than-expected annual pace of 2.8% in the third quarter.

Investors are watching closely the health of the US economy, with signs of growing strength likely to raise expectations that the US Federal Reserve will begin to scale back its massive economic stimulus programme.

Chris Williamson, chief economist at the researchers Markit, said that the jobs figure had “defied” expectations of a slump in jobs creation due to the shutdown.

“Analysts were expecting a mere 125,000 rise,” he said.

“The data will add to the view that the Federal Reserve is gearing towards a tapering of its asset purchases, but policymakers will most likely wait for clearer signs that the economy is capable of growing at a faster rate than seen in recent months, hoping to see a pace of economic growth that will eat into unemployment.”

In Thursday’s GDP figure, the Commerce Department said that growth had been lifted by rising exports and a pick-up in construction of homes.

However, it also said that the pace of growth in consumer spending – which accounts for about two-thirds of US economic activity – had slowed from the previous quarter.

Chris Williamson said: “The jobs report follows yesterday’s GDP numbers, and together the data suggest that the US economy continues to expand at a reasonable pace, but that the underlying rate of expansion has cooled since earlier in the year, when policymakers began talking in earnest about scaling back monetary stimulus.”

According to latest official figures, the US economy added 148,000 jobs in September, lower than analysts had predicted.

The unemployment rate fell to 7.2%, down from 7.3% in August, the US Department of Labor said.

The release of the figures was delayed by the partial shutdown of the US government earlier this month.

Economists had predicted 180,000 job gains for September, and the lower-than-expected figure could raise fears the US economy is losing momentum.

The US economy added only 148,000 jobs in September, lower than analysts had predicted

Employment in professional and business services grew at the fastest pace with 32,000 new jobs added. Leisure and hospitality was the only sector to see a fall with 13,000 jobs lost.

Following the figures, stock markets turned higher, with the FTSE 100 up 0.5% at 6,688 and both the Dow futures and broader S&P index futures up 0.3%, as investors bet on the Fed continuing its stimulus programme at the same pace.

The dollar fell, under pressure from the expectation that the stimulus programme, which effectively creates more dollars, will continue at the same rate.

The US central bank, the Federal Reserve, maintained its economic stimulus programme last month, suggesting it was still uncertain about the strength of the economic recovery.

The Labor Department said the next US unemployment data would be released on November 8, a week later than scheduled due to the partial shutdown of the US government.

Its workers were placed on unpaid leave during the shutdown raising fears the department will struggle to collect accurate data for October.

The seasonally-adjusted rate for April 2013 was 12.2%, up from 12.1% the month before.

An extra 95,000 people were out of work in the 17 countries that use the euro, taking the total to 19.38 million.

Both Greece and Spain have jobless rates above 25%. The lowest unemployment rate is in Austria at 4.9%.

The European Commission’s statistics office, Eurostat, said Germany had an unemployment rate of 5.4% while Luxembourg’s was 5.6%.

The highest jobless rates are in Greece (27.0% in February 2013), Spain (26.8%) and Portugal (17.8%).

In France, Europe’s second largest economy, the number of jobless people rose to a new record high in April.

“We do not see a stabilization in unemployment before the middle of next year,” said Frederik Ducrozet, an economist at Credit Agricole in Paris.

“The picture in France is still deteriorating.”

Eurozone unemployment rate has reached another record high in April 2013

Youth unemployment remains a particular concern. In April, 3.6 million people under the age of 25 were out of work in the eurozone, which translated to an unemployment rate of 24.4%.

Figures from the Italian government showed 40.5% of young people in Italy are unemployed.

“We have to deal with the social crisis, which is expressed particularly in spreading youth unemployment, and place it at the centre of political action,” said Italy’s President Giorgio Napolitano.

In the 12 months to April, 1.6 million people lost their jobs in the eurozone.

While the jobless figure in the eurozone climbed for the 24th consecutive month, the unemployment rate for the full 27-member European Union remained at 11%.

The eurozone is in its longest recession since it was created in 1999. At 1.4%, inflation is far below the 2% target set by the European Central Bank (ECB).

Consumer spending remains subdued. Figures released on Friday showed that retail sales in Germany fell 0.4% in April compared with the previous month.

Earlier this week, the Organization for Economic Co-operation and Development (OECD) predicted that the eurozone economy would contract by 0.6% this year.

According to Carsten Brzeski, an economist at ING, in the past, the eurozone has needed economic growth of about 1.5% to create jobs.

Some consider that the ECB needs to do more than simply cutting interest rates to boost economic activity and create jobs.

Earlier this month, the ECB lowered its benchmark interest rate to 0.50% from 0.75%, the first cut in 10 months, and said it was “ready to act if needed” if more measures were required to boost the eurozone’s economic health.

In its report earlier this week, the OECD hinted that the ECB might want to expand quantitative easing (QE) as a measure to encourage stronger growth.

The European Central Bank is due to meet next week.

France has entered its second recession in four years after the economy shrank by 0.2% in the first quarter of 2013, according to official figures.

The country’s economy shrank by the same amount in the last quarter of 2012. A recession is defined as two consecutive quarters of negative growth.

France has record unemployment and low business and consumer confidence.

German figures, also released, showed its economy, the eurozone’s strongest, grew by just 0.1% in Q1 2013.

France entered its worst recession since World War II in 2009. Although it was thought to have been in recession in 2012, these figures have now been revised to show only one quarter of negative growth.

The news comes on the first anniversary of Francois Hollande being sworn in as president.

Earlier this month, the European Commission warned that France would enter recession this year and said the eurozone’s economy would shrink by 0.4%.

France has entered its second recession in four years after the economy shrank by 0.2 percent in Q1 2013

The European Central Bank (ECB) cut interest rates at its last meeting to a record low of 0.5% in an attempt to stimulate growth.

In France, the rate of unemployment is running at 10.6% and is forecast to rise further next year.

Its deficit is also expected to rise sharply, the commission says, to 3.9% of GDP – well above the EU deficit target of 3%.

But French unemployment is below the eurozone average, which was 11.4% in 2012 and is expected to hit an average of 12.2% this year. In both Greece and Spain, it is expected to peak at 27%.

France this week passed a range of measures aimed at stopping the rise in unemployment by reforming the country’s labor laws.

These include measures to make it easier for workers to change jobs and for companies to fire employees.

The French economy has performed better than other eurozone members, including Spain and Italy, but it has not moved as quickly to reform its economy.

One of the new bill’s main measures is to allow companies to cut workers’ salaries or hours temporarily during times of sluggish economic performance, something that is common in Germany.

The figure for German growth, the largest and still the strongest economy in the 17-strong eurozone, was far weaker than expected. Economists had expected to see growth of 0.3% in the first quarter.

Annual figures from the Statistics Office also show the German economy has shrunk by 1.4% when compared with a year ago.

But in a statement it said this was partly due to severe winter weather: “The German economy is only slowly picking up steam. The extreme winter weather played a role in this weak growth.”

[youtube a7dUpDCz73I]

This website has updated its privacy policy in compliance with EU GDPR 2016/679. Please read this to review the updates about which personal data we collect on our site. By continuing to use this site, you are agreeing to our updated policy. AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.