Home Tags Posts tagged with "Economy of the United States"

Economy of the United States

The House of Representatives has passed an increase in the US government’s debt limit, after the Republicans gave up on their attempt to win concessions from the Democrats in return.

The House voted 221-201 to waive the $17.2 trillion debt limit for just over a year, with only 28 Republicans joining most of the Democrats.

Officials had said the US could breach the debt limit by the end of February.

The White House and others had warned of calamity if the US defaulted.

The bill, when signed into law by President Barack Obama, will enable the US government to borrow money to fund its budget obligations and debt service.

The US government will run a budget deficit of about $514 billion in its 2014 fiscal year.

The House of Representatives has passed an increase in the US government’s debt limit

The Republicans hold a majority in the House, and many had hoped to leverage their ability to block an increase in the government’s borrowing limit to win policy concessions from Barack Obama and the Democrats who control the Senate.

In the current and past debt limit fights, the Republican Party’s wish-list has included extensive budget cuts, measures that would repeal or undermine Barack Obama’s signature healthcare reform, a proposal to force the president to approve the Keystone XL oil pipeline from Canada, a repeal of recent cuts to pensions for working-age military retirees, and more.

“He will not engage in our long-term spending problem,” Republican House Speaker John Boehner told reporters earlier on Tuesday.

“So let his party gives him the debt ceiling increase that he wants.”

As in the last major Washington DC budget brawl, in September and October, Barack Obama and the Democrats said they would refuse to negotiate over the borrowing limit, arguing raising the limit amounted to the US government making good on spending it had already undertaken.

They demanded a “clean” bill that would raise the debt ceiling without enacting additional policy measures.

The Republican House leadership, often at odds with its restive caucus, floated a plan on Monday that would tie the debt limit increase to restoring a cut in pensions for working-age military retirees that was enacted as a money-saving measure in a recent budget.

But they found they lacked the Republican votes to pass that, as conservative members balked.

A separate vote is planned on that issue. The Senate has already passed a bill to restore the cuts.

[youtube 0JYKz391-Gw 650]

According to official figures, the US economy added 113,000 jobs in January, weaker than expected for a second consecutive month.

Economists had predicted an increase of about 180,000 new jobs last month.

However, the unemployment rate fell to 6.6%, the lowest level since October 2008, as more people began looking for work.

The US economy added 113,000 jobs in January, weaker than expected for a second consecutive month

The jobless figures will raise concern that, after a strong second half of 2013, growth in the US economy is beginning to lose its steam.

Earlier this week an unexpectedly weak manufacturing report raised concerns about the strength of the US economy and sent the Dow Jones tumbling by 326 points.

December’s surprisingly weak figure was revised up only modestly to 75,000, from 74,000.

The construction industry, most vulnerable to the impact of bad weather, added 48,000 in January indicating that while the weather may been responsible for December’s weak figures, it does not appear to have been a factor in January.

[youtube CLP1Y1_ju2c 650]

Treasury Secretary Jack Lew has warned the US may default on its debt by the end of the month if Congress does not raise its borrowing limit.

Jack Lew said he could rely on emergency measures to pay US debts after the limit is reinstated on February 7.

But he anticipated the treasury’s reserves would quickly be exhausted as it issues annual income tax refunds.

Congress suspended the debt limit in October as part of a deal to reopen the federal government after a shutdown.

The $16.7 trillion cap will be reinstated on Friday.

“Without borrowing authority, at some point very soon, it would not be possible to meet all of the obligations of the federal government,” Jack Lew said at the Bipartisan Policy Center in Washington on Monday.

Treasury Secretary Jack Lew has warned the US may default on its debt by the end of the month if Congress does not raise its borrowing limit

The treasury secretary said the US treasury department could resort to accounting mechanisms to avoid breaching the limit until the end of February.

But soon after, the US will only be able to pay its debt and other obligations with cash on hand.

And in the spring, Jack Lew noted, the US issues tax refunds to Americans who overpaid income taxes last year, straining its cash reserves.

While Republicans have in the past demanded budget cuts in return for agreeing an increase in the borrowing limit, the party’s leaders have signaled reluctance to do so this time around.

In any case, the White House has said it will not negotiate budget policy in exchange for raising the debt limit.

Jack Lew argued that dramatically cutting back on the federal government’s spending was unnecessary for the moment.

“I’m not sure this is the year for the long-term fiscal challenge to be dealt with,” he said, adding the US deficit had been declining.

“I actually believe that we’ve made so much progress in the short and medium term, we have a little time to deal with the longer term.”

During the partial government shutdown in October, Republican lawmakers threatened to block a rise in the debt limit unless the Democrats agreed to undermine or repeal President Barack Obama’s signature healthcare reform law.

The US jobless rate fell to a five-year low of 6.7% in December as companies created 74,000 new jobs, latest figures show.

However, the number of jobs created was the lowest for three years and was well under half the number expected by analysts.

The US had bad weather in December, which may have stalled hiring plans.

The fall in the rate, now at its lowest since October 2008, in part reflects people leaving the labor force.

The government counts people as unemployed only if they say they are actively searching for work.

The US jobless rate fell to a five-year low in December 2013

The leisure, manufacturing and services sectors added jobs in December, but construction cut 16,000 jobs, the biggest drop in the industry in 20 months.

In the four months before December, the average number of jobs created in the US was 214,000 a month.

Other figures on employment have suggested a healthy jobs market, and the Labor Department said 38,000 more jobs in November were created than the 203,000 previously reported.

Overall, the US economy is picking up steam, with recent figures for consumer spending, trade and factory output all strong.

This year, economists expect the US economy to grow by 3%, well up on the 1.7% last year.

The improving picture led the Federal Reserve to start to taper its massive monetary stimulus program from $85 billion a month to $75 billion.

If the Fed remains confident about the direction of the economy, it may trim this back further at its next meeting at the end of this month.

The meeting will be the last one chaired by Ben Bernanke, who will leave the post after eight years. He will be replaced by Janet Yellen on February 1st.

[youtube jh5M0uYu3gY 650]

Global stock markets rallied after the US Federal Reserve’s commitment to keep interest rates low offset its decision to taper its stimulus programme.

Germany’s Dax and France’s CAC were 1.5% in mid-morning trading, while the UK’s FTSE rose 1%. Japan’s Nikkei 225 closed up 1.7%.

The Fed said it would scale back its $85 billion a month bond-buying programme by $10 billion a month.

Analysts said the taper was less than markets had expected.

Investors and economists have been watching closely for when the Fed would scale back its stimulus, fearing that a steep taper could undermine economic recovery.

Global stock markets rallied after the US Federal Reserve’s commitment to keep interest rates low offset its decision to taper its stimulus programme

US markets had ended sharply higher on Wednesday following the Fed’s decision. The Dow Jones jumped 292.71 points, or 1.84%, to close at 16167.97, while both the Nasdaq and S&P 500 indexes rose by more than 1%.

The stimulus programme, called quantitative easing, was introduced by the Fed after the global financial crisis.

The main objective was to increase the money supply and improve liquidity in the financial system in the hope of sparking economic growth and supporting employment.

The Fed’s governing committee cited stronger job growth as a reason for the decision to begin winding down the programme.

It forecast the unemployment rate would fall to 6.3% in 2014 from its current level of 7%.

Analysts said the Fed’s decision to scale back the programme also indicated that it was confident of a sustained recovery in the US economy.

[youtube VstnJqU3E-A 650]

The US Labor Department has announced the unemployment rate fell to a five-year low of 7% in November.

Payroll figures also showed that 203,000 jobs were created last month, more than predicted, as the US economy displayed more signs of strength.

The monthly non-farm payroll figure is watched closely by economists.

Analysts say these indications of strong growth could mean that the Federal Reserve will start to unwind its massive stimulus programme soon.

However, the November figure might have been distorted. Some federal workers who were counted as jobless in the October – because of the 16-day partial government shutdown – returned to their jobs last month.

The latest data also showed that the October and September non-farm payroll figures, which had also been strong, were even better than their first estimates.

The US unemployment rate fell to a five-year low in November

Job gains for those two months were revised upwards by 8,000.

Chris Williamson, chief economist at research firm Markit, said the data indicated the US labor market was “buoyant”.

“The decline pushes the jobless rate down to its lowest since November 2008 and closer towards the Fed’s threshold of 6.5%, which it wants to see breached before it considers tightening policy via higher interest rates,” he said.

But he added that a decision on when the Fed might start to taper its stimulus programme was still not clear cut.

The labor market figures follow news earlier this week that economic growth, as measured by GDP, in the third quarter of the year was revised up to an annual pace of 3.6% from a previous estimate of 2.8%.

Also on Friday, the US Commerce Department said that consumer spending increased in October, though wages and salaries were barely changed.

According to the latest figures from the Labor Department, the US economy added a better-than-expected 204,000 jobs in October.

There had been fears that the 16-day shutdown of government services last month could have hit jobs growth.

The monthly non-farm payroll figure is taken as a key indicator of the health of the world’s biggest economy.

However, the latest figures also showed that the unemployment rate edged up to 7.3% from 7.2% in September.

The Labor Department said that this was likely to be because many federal workers were counted as unemployed during the shutdown.

The report also said that employers added 60,000 more jobs in September and August than earlier estimates had suggested.

The US economy added a better-than-expected 204,000 jobs in October 2013

The latest figures add to a positive week for US economic data.

On Thursday, it was announced that the US economy grew at a better-than-expected annual pace of 2.8% in the third quarter.

Investors are watching closely the health of the US economy, with signs of growing strength likely to raise expectations that the US Federal Reserve will begin to scale back its massive economic stimulus programme.

Chris Williamson, chief economist at the researchers Markit, said that the jobs figure had “defied” expectations of a slump in jobs creation due to the shutdown.

“Analysts were expecting a mere 125,000 rise,” he said.

“The data will add to the view that the Federal Reserve is gearing towards a tapering of its asset purchases, but policymakers will most likely wait for clearer signs that the economy is capable of growing at a faster rate than seen in recent months, hoping to see a pace of economic growth that will eat into unemployment.”

In Thursday’s GDP figure, the Commerce Department said that growth had been lifted by rising exports and a pick-up in construction of homes.

However, it also said that the pace of growth in consumer spending – which accounts for about two-thirds of US economic activity – had slowed from the previous quarter.

Chris Williamson said: “The jobs report follows yesterday’s GDP numbers, and together the data suggest that the US economy continues to expand at a reasonable pace, but that the underlying rate of expansion has cooled since earlier in the year, when policymakers began talking in earnest about scaling back monetary stimulus.”

[youtube wfDAnyaBEdM 650]

A federal jury has found Bank of America’s Countrywide Financial unit liable for defrauding two US government-backed mortgage companies.

Countrywide, which was acquired by Bank of America in 2008, was accused of selling thousands of defective loans to Fannie Mae and Freddie Mac.

The ruling is a major win for the US government, which launched the case in the wake of the financial crisis.

The Justice Department is seeking as much as $848 million in penalties.

The judge who presided over the trial said a civil penalty will be decided at a later date.

A former Countrywide executive Rebecca Mairone was also found liable on a civil fraud charge. She was the only individual to be sued by the government in the case.

The month-long trial focused on a Countrywide programme that was internally called “Hustle” or “high-speed swim lane” which allowed loans to be processed quickly without checking their quality.

The wrongdoing, which mostly took place before Countrywide was acquired, was discovered after a whistleblower filed a lawsuit against the firm.

Bank of America’s Countrywide Financial unit was found liable for defrauding two US government-backed mortgage companies

Manhattan US Attorney Preet Bharara welcomed the ruling.

“In a rush to feed at the trough of easy mortgage money on the eve of the financial crisis, Bank of America purchased Countrywide, thinking it had gobbled up a cash cow,” he said in a statement.

“That profit, however, was built on fraud, as the jury unanimously found.

“In this case, Bank of America chose to defend Countrywide’s conduct with all its might and money, claiming there was no case here. The jury disagreed,” Preet Bharara said.

Preet Bharara added that US authorities would “never hesitate to go to trial to expose fraudulent corporate conduct and to hold companies accountable, particularly when it has caused such harm to the public”.

The US economy witnessed a big boom in its housing market in the lead up to the 2007-08 global financial crisis.

As house prices continued to rise, many banks looked to cash in on the boom by creating complex financial products that grouped together home loans.

However, a collapse in the housing market saw the value of those investments plummet as the underlying mortgage holders became unable to repay their debts.

This snowballed into something called the subprime crisis, which hurt investors globally and caused billions of dollars in losses.

Since then, banks have been under pressure to resolve claims on potentially faulty mortgages.

The US Department of Justice is investigating at least nine banks over their sales of mortgage-backed securities.

[youtube HQAd4P7GV9M 650]

According to latest official figures, the US economy added 148,000 jobs in September, lower than analysts had predicted.

The unemployment rate fell to 7.2%, down from 7.3% in August, the US Department of Labor said.

The release of the figures was delayed by the partial shutdown of the US government earlier this month.

Economists had predicted 180,000 job gains for September, and the lower-than-expected figure could raise fears the US economy is losing momentum.

The US economy added only 148,000 jobs in September, lower than analysts had predicted

Employment in professional and business services grew at the fastest pace with 32,000 new jobs added. Leisure and hospitality was the only sector to see a fall with 13,000 jobs lost.

Following the figures, stock markets turned higher, with the FTSE 100 up 0.5% at 6,688 and both the Dow futures and broader S&P index futures up 0.3%, as investors bet on the Fed continuing its stimulus programme at the same pace.

The dollar fell, under pressure from the expectation that the stimulus programme, which effectively creates more dollars, will continue at the same rate.

The US central bank, the Federal Reserve, maintained its economic stimulus programme last month, suggesting it was still uncertain about the strength of the economic recovery.

The Labor Department said the next US unemployment data would be released on November 8, a week later than scheduled due to the partial shutdown of the US government.

Its workers were placed on unpaid leave during the shutdown raising fears the department will struggle to collect accurate data for October.

The US government is to reopen after Congress has passed a bill to raise the federal debt limit, with hours to spare before the nation risked default.

The Democratic-controlled Senate passed the measure by 81 votes to 18, and the Republican-controlled House of Representatives by 285 votes to 144.

Despite reluctant support from the House Republican leadership, most of the party’s lawmakers voted against it.

It came hours before the deadline to raise the $16.7 trillion limit.

The bill yanked the US back from the brink of a budgetary abyss by extending the treasury’s borrowing authority until February 7.

It also funds the government to January 15, reopening closed federal agencies after 16 days of partial government shutdown and bringing hundreds of thousands of employees back to work.

President Barack Obama signed the bill into law early on Thursday morning.

The US government is to reopen after Congress has passed a bill to raise the federal debt limit, with hours to spare before the nation risked default

The White House budget office said federal workers should return to work on Thursday.

The deal, however, offers only a temporary solution and does not resolve the budgetary issues that fiercely divide Republicans and Democrats.

President Barack Obama warned that US lawmakers must “earn back the trust of the American people”.

“We’ve got to get out of the habit of governing by crisis,” Democratic Barack Obama added, speaking after the Senate vote on Wednesday evening.

“My hope and expectation is everybody has learned there’s no reason why we can’t work on the issues at hand, why we can’t disagree between the parties without still being agreeable and make sure that we’re not inflicting harm on the American people when we do have disagreements.”

Also speaking after the first vote, Senate Democratic Majority leader Harry Reid said: “Let’s be honest, this is pain inflicted on a nation for no good reason and we cannot, cannot make the same mistake again.”

The US Treasury has been using what it called “extraordinary measures” to pay its bills since the nation reached its current debt limit in May.

It said those methods would be exhausted by October 17, leaving the US unable to meet all of its debt and other fiscal obligations.

Politicians, bankers and economists had warned of dire global economic consequences unless an agreement to raise the US government’s borrowing limit was reached.

Meanwhile, ratings firm Standard & Poor’s said on Wednesday that the partial US government shutdown, the first in 17 years, had already shaved $24 billion from the American economy and would cut growth significantly in the fourth quarter.

[youtube 4Wd7xhFd8bo 650]

Democrat and Republican leaders of the Senate have struck a cross-party deal to end a partial government shutdown and raise the US debt limit.

Their bill must also pass the House, where a small group of Republicans are expected to join Democrats to send the bill to President Barack Obama.

The bill extends the federal borrowing limit until February 7 and funds the government to January 15.

The move comes just a day before the deadline to raise the $16.7 trillion limit.

Democrat and Republican leaders of the Senate have struck a cross-party deal to end a partial government shutdown and raise the US debt limit

On the floor of the Senate, Democratic leader Harry Reid called the legislation “historic”, saying it would provide time for Congress to work toward a long-term budget agreement.

“Our country came to the brink of disaster,” Harry Reid said.

Republican Senate Minority Leader Mitch McConnell, Harry Reid’s negotiating partner, said he was “confident” the government could reopen and avoid default under the proposed bill.

“Now it’s time for Republicans to unite behind other crucial goals,” Mitch McConnell said.

[youtube HVYCRCsPLQU 650]

JP Morgan will pay $100 million to settle with the US Commodities Futures Trading Commission over losses stemming from its “London Whale” trading debacle in 2012.

In a first, JP Morgan will admit that its traders acted “recklessly”.

The CFTC says the trades, which ultimately cost the bank $6 billion in losses, distorted prices in the market.

Last month, the bank agreed to pay $920 million to other regulators in the US and the UK over the bad trades.

JP Morgan will pay $100 million to settle with the US Commodities Futures Trading Commission over losses stemming from its “London Whale” trading debacle in 2012

The scandal arose from disastrous trades by former bank employee Bruno Iksil, who earned the nickname of the “London Whale” for his big bets on the financial markets.

David Meister, the head of enforcement at the CFTC, said in a statement that the traders tried “to <<defend>> their position by dumping a gargantuan, record-setting volume of swaps virtually all at once, recklessly ignoring the obvious dangers to legitimate pricing forces”.

The bank has found itself overwhelmed by mounting legal troubles lately.

Once the darling of Washington and Wall Street, it reported a rare quarterly earnings loss last week, mostly due to legal costs totaling $9.2 billion.

The bank lost $380 million during the quarter, compared with a profit of $5.7 billion in the same period last year.

JP Morgan says it has set aside a fund of $23 billion to deal with mounting legal costs relating not just to the “London Whale” trading debacle, but also to charges that the bank misled consumers and investors during the housing market collapse.

US media has estimated that JP Morgan could be negotiating a settlement of several billion dollars with a variety of US regulators.

An announcement of this settlement – surely the largest banking fine in US history – is expected to be announced soon.

World Bank’s President Jim Yong Kim has warned that the US is just “days away from a very dangerous moment” because of the government’s borrowing crisis.

Jim Yong Kim urged US policymakers to reach a deal to raise the government’s debt ceiling before Thursday’s deadline.

The US Treasury will start to run short of funds if no agreement is reached for it to borrow on financial markets.

Jim Yong Kim urged US policymakers to reach a deal to raise the government’s debt ceiling before Thursday’s deadline

Jim Yong Kim warned this could be a “disastrous event” for the world.

“The closer we get to the deadline the greater the impact will be for the developing world.

“Inaction could result in interest rates rising, confidence falling and growth slowing,” he said speaking at the World Bank’s annual meeting in Washington.

“If this comes to pass it could be a disastrous event for the developing world and that will in turn greatly hurt the developed economies as well,” Jim Yong Kim added.

[youtube y5p_btwtm4I]

The US shutdown negotiations have been shifted to the Senate.

The Democratic and Republican leaders in the Senate held direct talks for the first time in weeks, but there is little sign of any breakthrough, correspondents say.

The shutdown began when Congress missed the October 1st deadline to pass a budget.

The US faces another deadline on Thursday to raise its debt limit.

If a deal is not reached by then, the US faces potential default, a prospect which has caused alarm both domestically and abroad.

Senator Dick Durbin, a Democrat, said the aim was to reach a deal on extending the debt limit before markets reopen on Monday.

The talks between Senate Majority Leader Harry Reid and Senate Republican leader Mitch McConnell earlier on Saturday represented the first face-to-face meeting between the two since July, the New York Times reported.

“The conversations were extremely cordial but very preliminary of course – nothing conclusive, but I hope that our talking is some solace to the American people and to the world,” said Harry Reid.

The US shutdown negotiations have been shifted to the Senate

“We had a good meeting,” said Mitch McConnell, without elaborating.

Harry Reid then went to the White House for talks with President Barack Obama.

But he rejected a plan put forward by Republican Senator Susan Collins to allow the government to increase its debt limit until January 31st, 2014.

Democrats have a majority in the Senate, but could not muster enough support to advance a proposal to lift the debt ceiling there.

Talks between House Republicans and the White House had collapsed earlier.

Republicans have refused to pass a new budget unless President Barack Obama agrees to delay or eliminate the funding of the healthcare reform law of 2010.

Hundreds of thousands of federal employees have been sent home as a result of the shutdown.

The White House has repeatedly said it would not undermine the law, known as Obamacare, nor negotiate over larger budget matters, until Republicans vote to end the threat of default.

It has also rejected a short-term deal over the debt limit.

“It wouldn’t be wise, as some suggest, to just kick the debt ceiling can down the road for a couple of months, and flirt with a first-ever intentional default right in the middle of the holiday shopping season,” President Barack Obama said.

[youtube OYyHz-wAkvg]

Asian markets have risen on hopes the US will reach a deal on raising its debt ceiling, tracking overnight gains on Wall Street.

This was after Republicans from House of Representatives offered President Barack Obama a short-term increase in the debt limit to stave off default.

Stock indexes in Japan, Australia, China and Hong Kong all gained.

There have been concerns that a failure to agree a deal to raise the limit may see the US default on its payments and hurt the global economy.

Analysts said the offer by the Republicans had raised hopes that such a scenario was likely to be avoided.

Asian markets have risen on hopes the US will reach a deal on raising its debt ceiling, tracking overnight gains on Wall Street

“What this is, is opening the door to discussion and negotiation when before we had two sides just finger pointing,” said Peter Jankovskis, co-chief investment officer at OakBrook Investments LLC.

“We don’t know if in six weeks we’ll be in the same place, but at least this opens the possibility [of a deal]”, he said.

Japan’s Nikkei 225 index rose 1.5%, Hong Kong’s Hang Seng gained 1.3%, Australia’s ASX 200 added 1.6% and South Korea’s Kospi was up 1.2%.

On Thursday, the US markets had their best day since January 2013, buoyed by the proposal. The Dow Jones, S&P 500, and Nasdaq indexes all closed up by more than 2%.

The US needs to agree on raising the nation’s $16.69 trillion debt ceiling by October 17.

A failure to do so could see the US government default, as it runs out of money to pay its bills and service its national debt.

[youtube u2-bl2Bzb9c]

Republicans in the House of Representatives have met President Barack Obama amid renewed efforts to avert a looming debt crisis.

Both sides described the 90-minute meeting as useful but said no decision was made. They agreed to keep talking.

Republicans have offered the president a short-term debt limit increase to stave off default.

A new poll suggests the majority of Americans blame the Republicans for the partial shutdown of government.

A Wall Street Journal/NBC News poll suggests 53% of Americans blame the Republicans for the crisis, compared with 31% who say the Democrats are responsible.

“It was a very adult conversation,” said Republican Hal Rogers of the meeting.

“Both sides said they were there in good faith.”

House Majority leader Eric Cantor called the meeting “very useful” and said the talks were continuing.

The White House said in a statement: “The president looks forward to making continued progress with members on both sides of the aisle.”

Officials have warned the US risks default on October 17 if the nation’s borrowing limit is not increased.

Republicans in the House of Representatives have met President Barack Obama amid renewed efforts to avert a looming debt crisis

Republicans have offered to extend the government’s borrowing authority beyond the deadline, temporarily putting off a default.

In return they want Barack Obama to further negotiate on the budget dispute that has partially closed the government – the first shutdown for 17 years.

It is not clear if Republicans are willing to drop entirely their attempts to defund or delay Barack Obama’s 2010 healthcare law.

Leading Republican Pete Sessions said the two sides were working on “defining parameters to see if we can make progress”.

Earlier, House of Representatives Speaker John Boehner said Republicans had told Barack Obama they wanted “a temporary increase in the debt ceiling” followed by talks on “a way forward to reopen the government.”

“It’s time for leadership,” the Ohio Republican said.

“It’s time for these negotiations and this conversation to begin.”

A spokesman for John Boehner told reporters the deal offered was a “clean” increase of the debt limit, with no additional policies attached.

It would only last six weeks – until November 22.

Reacting to the offer, White House press secretary Jay Carney told a daily press briefing the president was glad that “cooler heads” seemed to be prevailing in the House.

But he added: “He will not pay ransom in exchange for the Republicans in the House doing their job.”

Earlier on Thursday, Democratic Senate leader Harry Reid said the Senate would “look at anything” the House sent to them, but they would not engage in negotiations with Republicans prior to reopening the government.

The impasse over the debt limit has already rattled markets and increased the interest rate for one-month US Treasury bills. But US stock markets rebounded on Thursday on news of a possible breakthrough.

Democratic Senate finance committee chairman Max Baucus said the Republican campaign to undermine the healthcare law in return for agreeing to end the shutdown was “not up for debate” and would not happen.

Hundreds of thousands of federal employees have been out of work since the shutdown began, and private firms, from arms makers to motels, have begun to lay off workers.

About 15,000 private-sector employees have filed for unemployment benefits due to the shutdown, the US labor department said on Thursday.

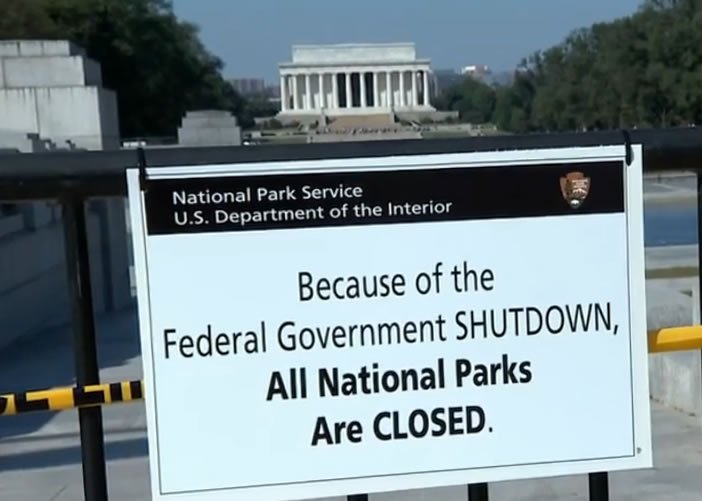

And governors in at least four western states – Utah, South Dakota, Arizona and Colorado – have asked for authority to reopen national parks within their borders because of the economic impact of the closures.

On Thursday, Barack Obama signed legislation restoring death benefits to families of US troops who have died since the government closed. The shutdown prevented processing of the payments, typically made within days of the soldier’s death.

The president also met House Democrats at the White House on Wednesday and told them he would prefer a longer-term increase to the nation’s $16.69 trillion debt ceiling.

But the president said he was willing to accept a short-term rise in the borrowing cap to “give Boehner some time to deal with the Tea Party wing of his party”, Representative Peter Welch told the Associated Press news agency after the meeting, referring to a Republican faction of hard-core conservatives.

Earlier, Treasury Secretary Jack Lew told a congressional panel that skipping a payment on US debt would trigger a potentially profound financial crisis.

“It would be chaos,” Jack Lew told the Senate hearing.

Since the US hit its debt ceiling in May, the treasury has been using what are called extraordinary measures to keep paying the bills, but those methods will be exhausted by October 17, Jack Lew has said.

[youtube wpm3bRPP-Ok]

President Barack Obama has announced he is willing to hold budget talks with Republicans, but not until they agree to lift “threats” against the economy.

Republicans “don’t get to demand ransom in exchange for doing their jobs”, Barack Obama said, by demanding concessions in policy before reopening government.

The US government shut down last week when Congress failed to agree a budget.

Republican leaders on Tuesday renewed their calls for Barack Obama to open negotiations over ending the impasses.

Republican House Speaker John Boehner told reporters he was “disappointed that the president refuses to negotiate”.

He said the president’s position not to talk with Republicans “until [they] surrender” was not sustainable, and any discussions regarding the debt ceiling must address how the nation is “living beyond its means”.

At the White House, Barack Obama said he had spoken to John Boehner and was “happy to talk with him and other Republicans about anything”.

But Barack Obama said any negotiations on the ongoing government shutdown or the debt limit “shouldn’t require hanging the threats of a shutdown or economic chaos over the heads of the American people”.

Barack Obama has announced he is willing to hold budget talks with Republicans, but not until they agree to lift “threats” against the economy

“We can’t make extortion routine as part of our democracy,” Barack Obama said.

“Democracy doesn’t function this way. And this is not just for me. It’s also for my successors in office, whatever party they’re from.”

He also warned of the repercussions of defaulting on the government’s debt should Congress fail to raise the borrowing limit, currently set to be reached on October 17.

Barack Obama said breaching the borrowing limit could disrupt capital markets, undermine international confidence in America, permanently increase the nation’s borrowing costs, add to its deficits and debt, and pose the “significant risk of a very deep recession”.

The US government partially shut down operations on October 1st after Republicans who control the House of Representatives refused to approve a budget, saying they would only do so if Barack Obama’s healthcare reform law were delayed or stripped of funding.

Barack Obama and the Democrats have thus far refused, noting the law was passed in 2010, subsequently approved by the Supreme Court, and was a central issue in the 2012 election which Obama won.

At the same time, the Republicans have refused to approve an increase in the US debt limit unless it is accompanied by significant spending cuts and other policy concessions.

Barack Obama maintains John Boehner could end the current government showdown by allowing the House to vote on a “clean” budget bill that does not alter the health law, because that could pass with votes from both Democrats and moderate Republicans.

But doing so would risk damaging his standing with the most conservative elements of his caucus, analysts say.

US and foreign officials and economists have warned of severe economic consequences if the US defaults on its debt because the government is unable to borrow money to fund its obligations.

[youtube W88GSw0hr8k]

Chinese Vice Finance Minister Zhu Guangyao has warned that the “clock is ticking” to avoid a US default that could hurt China’s interests and the global economy.

China, the US’s largest creditor, is “naturally concerned about developments in the US fiscal cliff”, Zhu Guangyao said.

Washington must agree a deal to raise its borrowing limit by October 17, or risk not being able to pay its bills.

Zhu Guangyao asked that “the US earnestly take steps to resolve” the issue.

US Treasury Secretary Jacob Lew has said that unless Congress agrees an increase in the debt ceiling by October 17, Washington will be left with about $30 billion in cash to meet its obligations – about half the $60 billion-a-day needed.

China, the US’s largest creditor, is naturally concerned about developments in the US fiscal cliff

For many governments and investors the approaching deadlock over the debt ceiling is far more critical than the current impasse over the federal shutdown caused by Congress’s failure to agree a new budget.

On Sunday Republican House Speaker John Boehner reiterated that Republican lawmakers would not agree to raise the debt ceiling unless it included measures to rein in public spending.

Zhu Guangyao said that China and the US are “inseparable”. Beijing is a huge investor in US Treasury bonds.

“The executive branch of the US government has to take decisive and credible steps to avoid a default on its Treasury bonds,” he said.

“It is important for the US economy as well as the global economy.”

“We hope the United States fully understands the lessons of history,” Zhu Guangyao said, referring to a similar deadlock in 2011 that led to a downgrade of the US “AAA” credit rating.

That deadlock ended with an eleventh-hour agreement.

[youtube fun-FYTdK9U]