There are several reasons behind someone having their license revoked or suspended. It includes driving without insurance, receiving driving offenses related to alcohol or drug, repeated traffic offenses, or failing on child support. Whatever the reason might be, getting vehicle insurance is easier with the help of a cheap car insurance company.

Although you cannot drive legally without a driver’s valid license, you still require low-cost auto insurance in most cases, irrespective of whether your license is revoked or suspended. But, getting the right insurance policy becomes hard. You may have limited options and may not avail of cheaper car insurance rates if you have a suspended or revoked license.

Photo Source: duidirectory.wordpress.com

Can you avail of car insurance with a suspended license?

Surely, you can get vehicle insurance irrespective of whether your license is suspended. Owning a car across several states requires you to be insured and tagged even though your license is revoked or suspended. It is a challenging affair with a suspended license as you cannot get rated as a driver on your policy if you cannot drive legally.

You can be banned as a driver till your license is reinstated or when a restriction is sanctioned. There are some ways to get car insurance with your license revoked or suspended:

Rating a household member having a clean driving record as a driver to your policy, although it might not be an option with almost every insurance company.

Getting approval for the restricted or hardship driver’s license allows you in driving at special situations like school or work.

Buy the SR-22 insurance.

If the car ownership is in someone else’s name, you insure it under their vocation.

Is your suspended license visible to the car insurance companies?

Surely, the car insurance companies can check whether your license is revoked or suspended. There are motor vehicles separated in your state notifying your insurance company electronically in the same manner when they are convicted of a moving violation or a ticket.

Suppose the insurance company gets the notification for the suspended license. In that case, the company might issue a nonrenewal or a cancellation of the insurance policy, although you are not near the renewal period. The company would also provide an exclusion allowing the insurance policy to be active; however, it needs the policyholder to sign a form that excludes you from the coverage. If you get into an accident, your car will not cover it.

Lowering car insurance coverage with license suspended.

You may have to carry complete coverage of insurance that meets lender requirements as your license is suspended if your car is leased or financed. You may purchase less coverage due to the cost of the car insurance if your vehicle is outright. Make sure to consider the risk associated with your vehicle and are you making the right choice by removing the collision or comprehensive insurance.

We recommend that you buy the only-comprehensive coverage if you plan to store your car untagged. But, if your car is tagged, you would need to meet the minimum liability insurance needs for the state, avoiding penalties and fines irrespective of the driver’s license status.

What can be done to get car insurance with a suspended license?

You will risk having your license suspended and getting caught driving without insurance, and you will have to buy car insurance before having your driving privileges restored if it happens. Not all companies will insure with the one having a license suspended. If you are classified under the high-risk driver, then it can result in you paying higher premiums.

If the driver’s license is suspended and you would have to purchase insurance, then here is what you should do:

● Applying for a hardship or restricted license

Several insurance companies do not insure someone with a suspended license; however, they would if you have a restricted or a hardship license. Some laws vary in each state. Make sure to check with the Department of Motor Vehicles in your state to determine whether you are eligible to apply for the restricted or hardship driver’s license.

● Shop for cheap insurance

The drivers classed as high-risk will have to pay a bit high premiums, and not every company will be insuring them. You can get the best rate on your car insurance with a suspended license by comparing the quotes.

● Avail an SR-22 or FR-44

Your insurer may have to file for a certificate of financial responsibility in respect to your state to prove you carry the much-needed minimum amount of liability insurance.

Final thoughts

It can result in a massive setback when your driving privileges are revoked or suspended. Getting affordable car insurance from a cheap car insurance company with a suspended license will involve work. Can you expect to find your insurance rates hitting the skies? You can get help, although most insurance companies will not offer you a policy with your suspended license. Additionally, shopping for car insurance online may be a bit hard, so you should directly speak to your insurance agents. You can even ask them in regards to the recommendations for this situation.

Guess what? You are the only perfect driver. Admit it; you have thought this before. Seriously though, no matter how vigilant you are, accidents happen.

Car accidents are scary no matter who’s at fault. There is an adrenaline rush, chaos, and sometimes you know what happened and sometimes you don’t. Your first instinct may be to jump out of your vehicle to find out what happened. Don’t do this.

Before getting to what to do in case of an accident, let’s talk about exactly what insurance is.

Basically, a car insurance policy protects you from paying for any damage or injuries if there is a car accident. Depending on the type of car insurance you have, it may cover damage to your car as well. Car crashes aren’t the only type of accidents that insurance covers. They also cover other things, such as hitting a stationary object like a tree, pole, or even your garage. Not to mention any animals that you aren’t able to avoid, like a deer.

Now, let’s get into what you really want to know. These steps work no matter who is at fault or even if you were involved in a hit and run. If you follow the steps, below you’ll discover filling out your paperwork is much easier when you know what to do if you’re in a car accident.

1. Check Yourself And Passengers For Injuries

Immediately check yourself and anyone that’s in the car for injuries. If anyone experiences neck or back pain, make sure they don’t move until help arrives. The adrenaline experienced in a car accident dulls your pain, and you may not realize the extent of the injury.

2. Check Your Surroundings & Get Out Of The Way Of Traffic

If there weren’t any injuries, check your surroundings and then move to safety. Check for the smell of gas and determine if you need to do anything to ensure everyone is safe. If you are in the way of traffic you need to move your car as long as there are no injuries.

While moving your vehicle, make sure you do it slowly and do your best to be calm. This is harder than you may think. Anyone who has been in an accident knows you can easily pull forward instead of reversing. These types of mistakes are common when you are in a high-stress situation. So really pay attention to what you’re doing to prevent further damage to your vehicle or the other party’s car.

3. Call The Police & Make A Report

No matter how minor the accident is, you need to call the police. If you are planning to file a claim with your insurance, a police report is mandatory. There are areas where police will not come out to a minor accident, especially in large cities.

When or if the police come out, you want to get their name, badge number, and contact information. You’ll also need to get a copy of the police report. Many places are moving their records online, and you’ll have to get your info off the internet. This will save time because if you don’t get it, your insurance company will have to.

4. Gather Information & Take Pictures

Especially if the police don’t show up, you’ll want to gather the other party’s information. You’ll need information such as their name, address, phone number, insurance information, and if there are any witnesses, you’ll need theirs too. As a side note, avoid discussing who’s at fault; stick to the facts.

If you have your cell phone with you, you need to take pictures of the vehicles and any injuries you or your passengers may have. There are times you may not be able to take the photos at the time of the accident. If not, then take them as soon as you can.

5. Seek Treatment & Notify Your Insurance Company

You must tell first responders about any pain you are experiencing after the accident and seek medical treatment immediately. You may not feel pain or think your injuries are minor but then experience pain a few days later. Having proper documentation will help prove the injury occurred due to the accident. If you experience new or worsening pain, you’ll want to immediately schedule an appointment with your doctor.

Sometimes people believe it is easier to negotiate a cash settlement with the other driver to avoid getting the insurance companies involved. This is a bad idea; You are liable for any damages above the cash settlement if you don’t contact your insurance company. Many states have a time limit on how long you can wait to file a claim, so it’s essential to do it immediately.

Most people think of car insurance as that useless bill you have to pay monthly… until you actually need it. You never know when or if an accident will happen, so make sure you have car insurance that best suits your needs and at a fair price. If you live in a no-fault state and don’t have car insurance, you can end up in a whole mess of trouble, especially with the law.

The steps listed above may seem like common sense, but you’d be surprised at how many people get lost in the heat of the moment. The truth is, many people act without thinking, and they instantly want to confront the other driver. Confrontation is something you want to avoid. Take the time to assess and breathe before doing anything foolish.

When looking into car insurance plans, the variety of options, prices, and coverage may cause confusion. The overwhelming amount of information can cause car owners to not fully understand the coverage that works best for their car, causing them to either be too covered or undercovered.

As you go through the car insurance process, you’ll need to ask a few questions to yourself and a representative to get the full picture. We’ll go over five of those questions in this article to help you better understand exactly what coverage you need and what you are able to afford.

What type of driver are you?

There are car insurance plans that cater to all types of drivers. When purchasing your plan, you need to ask yourself what you’ll be using your car for primarily. Do you use it for long road trips? To commute to work daily? Casually? Or, is it a car that needs a special type of coverage, such as an antique car?

Whatever your circumstances are, you’ll need to ask an insurance representative which type of coverage is best for you. For example, people who tend to drive on the safer side prefer a plan from Nationwide car insurance, as they offer benefits for those who drive safely.

How much can you afford?

Depending on your car and circumstances, your auto insurance premiums can increase or decrease. Typically, the nicer car you have, the more your premiums will be. Or, if you have a past accident on record, your premiums can increase as well. Other factors for price increases may include the type of coverage you choose, your location, the number of drivers on your policy, and more.

Make sure you can afford the coverage you choose before purchasing a plan. But, don’t cheap out on insurance either just to save a few dollars every month, as an accident can end up costing you more in the long run.

What type of coverage do you need and who is covered?

There are different types of coverage for auto insurance plans. The main types include:

Auto liability coverage

Collision coverage

Uninsured and underinsured motorist coverage

Personal injury protection

Medical payments

Comprehensive coverage

You can learn more about the specifics of each coverage by researching the basics of auto insurance. Based on where you live, some types of coverage may be required — or not. There are also different minimum coverage amounts required in every state. As you get ready to purchase an auto insurance plan, make sure you have all the coverage you need for your car and driving habits.

Are there any possible discounts?

Many auto insurance companies offer a variety of discounts for their policyholders. Some discounts may include student discounts, safe driver discounts, military discounts, bundled discounts, low mileage discounts, training discounts, auto-pay discounts, and more. Simply ask a representative what discounts may be available.

What is your risk assessment?

You should understand what your risk assessment is before purchasing an auto insurance policy. Risk assessment is the way policymakers determine how much of a risk you and/or your car holds as a policyholder. This is based on demographics, driving records, the car itself, and more. Your risk assessment will help the insurance company determine how much to charge you every month.

Once you determine the answers to these five questions, you’ll be able to understand what auto insurance policy you’re purchasing much better. The more you know about auto insurance plans, the easier it will be to make claims, changes, and payments in the event of an accident.

You might believe you got a good

deal when you pay a meager price for a salvaged car. However, such cars have

probably been rebuilt after being utterly destroyed in an accident. Car

insurance companies usually quote higher premium rates to insure these rebuilt

vehicles. Some automobile insurance agencies will not insure a salvaged car

while others offer liability coverage. Very few insurance companies provide

full coverage for such cars as it is difficult to assess all damages to the

vehicle.

What Does It Mean When A Car Has A Salvage

Title?

A

salvage title, also popularly known as a branded title, is issued to a vehicle

after it has been labeled as a total loss.

This is the opposite of a clean title which is what cars that have never

suffered severe damage are issued. If a vehicle suffers extreme damage and the

cost of repair is more than a certain percentage of the cars cash value, a

total loss has happened. Different automobile car insurers in different states

use varying levels as a benchmark for the total loss, but the value ranges

between 90% and 60%.

Once

a car insurance company makes a total loss declaration and issues a salvage

certificate, the car can no longer be registered and can no longer be driven on

public roads. Insurance companies typically go on to auction salvaged cars off

to salvage yards or rebuilders. If a salvaged car is rebuilt correctly and

passes the necessary tests, a rebuilt certificate can be issued for it. If the

vehicle was restored but still declared unfit to drive, it is given a

non-repairable title instead. Such a vehicle can never be driven again and is

only used for parts or dumped altogether.

Does A Salvage Title Affect The Price Of Car

Insurance Premiums?

There

are varied reasons why the premium rate for car insurance will increase.

Typically, the elements that cause premium rates to increase depending on how

high risk the policyholder is. According to car insurance companies, driving a

salvaged car makes you a very high-risk client. For this reason, premium rates

for salvaged vehicles tend to be much higher than average.

A car

can only be issued a salvage title if it passes inspection after rebuilding.

But there could be many defects hiding in covered areas, waiting to manifest at

the slightest encouragement. Such errors could even lead to unfortunate

accidents, and that is the biggest concern of auto insurance companies.

Another

reason most insurance companies will not touch a salvaged car with a 6-foot

pole is they are difficult to value. Comprehensive collision insurance might be

a good deal for your salvaged car, but since your insurance provider finds it

hard to value the vehicle, you should expect costly rates. Other insurance

covers, including uninsured motorist and liability insurance, might not cost

more than usual because the value of the car is not considered for determining

premium rates.

Is It Worth It To Buy Full Coverage On A Salvage

Car?

The search for an

auto insurance company that will cover a salvaged car is only the beginning;

getting a reasonably priced quote is another ball game. While some people

prefer to have full coverage, even for salvage title cars, some wonder if it is

worth it. Car insurance companies generally estimate standard cars value lower

than expected. You can assume that this will be lower for salvaged vehicles.

Only about 80% of the cars salvage value will get to you.

Another

consideration when contemplating full coverage for salvaged cars is that your

vehicle starts worthless. Insurance is usually paid out based on the value of

the car involved, so get ready to be paid much less if your salvaged car is

badly damaged in the future.

Conclusion

Cars with a salvage title are typically much cheaper than conventional vehicles. A lot of professionals advice car buyers to avoid buying salvaged cars or rebuilding total loss cars but these cars can still be driven and insured. Some car insurance companies will not provide coverage for salvaged cars, some only offer limited liability, but a few can offer full salvage title insurance coverage for vehicles with salvage titles.

If you have done proper research

and decided to buy and use a salvaged car long term, you can be covered by

individual car insurance firms. You should ask your car insurance provider

about their stance on insuring salvage cars. Also, inquire about additional

coverage you may be able to get with their regular packages. If you can find a

provider with a good deal, go ahead and make an offer. Make sure you have

confirmed that there will be no severe limitations for filing a claim with a

salvage title car before you go ahead. Your insurance provider might even

negotiate the value of the vehicle with you to provide you with the best

premium rates possible.

Nobody wants to be known for designing cars that people

crash. But cars used to be designed to look beautiful, rather than promote the

safety of their occupants. These days, manufacturers put their resources

towards making a safe car, right at the start of the design process.

There is a huge difference in safety between the best and the worst cars. In fact, a driver in the least safe car is 10 times more likely to be seriously injured or killed than in the safest car. So what makes a car safe? There are three elements: good structure, passive safety and safety assist technologies.

The structure of a car is its shell, and this is the main

protector. It has to withstand the force of a crash and channel those forces

away from all occupants. A good structure will protect the driver and

passengers and have effective crumple zones to absorb the energy of the crash.

During a crash, a safe car cabin can maintain its shape. The

steering column, dashboard, roof pillars, pedals and floor panels do not push

too much inwards. Doors remain closed, but can be opened afterwards for quick

rescue. Side door strength, padding and seating all protect from common, side

impact crashes.

Passive Safety Features

Well-designed cars now have built-in safety features,

such as airbags, ABS brakes, electronic stability control, seat belts and seat

belt pre-tensioners to manage the forces of impact. While airbags have been

around a long time, they have become a lot more sophisticated.

Always look for front, side,

curtain and knee pedestrian airbags for maximum safety. For example, head-protecting side airbags such

as curtain airbags, work well in side impact crashes and rollovers.

Safety Assist Technologies

Advanced driver assist (ADAS) technologies actively help

to prevent or reduce the severity of a crash. They may be semi-autonomous or

fully autonomous. For example, intelligent speed adaptation (ISA), blind spot

monitoring (BSM) autonomous emergency braking (AEB) and active lane keep assist

(LKA). Note manufacturers currently use different terms for the same kinds of

systems, which can be confusing.

Crash Testing

How do we know some cars are safer than others? From the

results of crash testing. US Insurance

Institute for Highway (IIHS) and Australasian New Car Assessment Program

(ANCAP) are two bodies that routinely conduct crash tests and award star

ratings.

IIHS front-end crashed a 1997

Pontiac Trans Sport/Chevrolet Venture. The door frame buckled, the steering

wheel pushed into the driver’s face and the cabin completely collapsed. After a

redesign in 2005 using high-tensile strength materials and a more rigid

structure, crash forces dissipated through the floor. The engine slid under the

vehicle rather than into the driver.

ANCAP compared two models of Toyota Corolla 5-door

hatchback, one built in 1998 and one in 2015. The latest model has six airbags,

ABS, electronic brake force distribution and brake assist as standard. 1998 has

none of these. The 1998 model crumpled heavily with extreme risk of serious

head, chest and leg injury to driver and scored 0 stars. The 2015 model had

minimal damage and scored 5 stars.

Design Saves Lives

Nobody wants to see a member of their family or a friend get hurt in a crash. We know the design of a car is crucial to keeping the driver and occupants safe. Moreover, most insurers reward people who drive safer cars with lower premiums. Safer cars help protect the vulnerable people around you, who are innocently going about their business.

It is worth buying a car that is not only designed to be

beautiful, but keeps everyone safe.

Car insurances give you the confidence and the much-needed protection when you are on the road. Depending on the age of the vehicle your needs might change, but no way does it negate the importance of auto insurance that you must have. For your own protection, as well as others around you, investing in a high-quality car insurance is imperative: insurance that would have your back when you would need it the most.

However, before you go looking

for an auto insurance, there are a few things you need to know first.

Car Insurance Rates Get Affected by Many Factors

You might not have known this, but there are plenty of factors that will come

to play a huge role in the car insurance deal you will finally get to sign on.

Some of them have been listed below for guidance:

Driving record: Your driving history, any previous violations or

accidents will be considered since they

put you at a higher risk

Age and gender: Men tend to have more accidents than women

Use of vehicle: People who have a higher annual mileage

automatically put their vehicles to more

risks

Model of the car: This is what would determine the number of claims

you will make in future

Each Auto Insurance Company is Different

Auto insurance is an extremely

competitive business where you would hardly ever find two companies offering

the same insurance price. Each one in the business

adopts its own policy for risks

calculations and can come up with a value that might vary by hundreds of

dollars from the others in the market. This

is why you need to be very careful about what you really want and research before you dive in.

Not All Coverages Are Expensive

The liability coverage that you

are bound to buy by law is the most expensive one of all followed by collision

coverage. The others that offer great

coverage without damaging your accounts include roadside assistance, gap

coverage and comprehensive coverage which covers the car you have for acts

involving fire, theft, and vandalism.

Ask for Discounts

There are a lot of things that you can do to earn some discount on the insurance package you are buying. Installing anti-theft devices, keeping a low mileage along with a good driving record, taking up education courses to improve your driving are just some of them. Make sure you discuss the prospects with your company and work to prove yourself as a better risk candidate to avail such offers.

Read Before You Sign

Since an auto insurance is a

legal contract, you should always review and thoroughly read it to make sure

that all that was discussed verbally has

made it to the final document. In case of any doubts, do discuss it with your

dealer without any delay.

If you are looking for a reliable company that would provide you with the best insurance deal, then, click “here” and find the answer you are looking for. Not only do they provide exemplary customer support but they also offer the lowest prices in town. Head over to the website today for more information.

On August 23rd, 2018 Detroit Mayor Mike Duggan and eight other residents of the Motor City appeared in federal court alleging that the current Michigan no-fault auto insurance laws requiring drivers to pay for this type of coverage is a violation of due process. At the same time, they claim this law is unconstitutional.

In the Eastern District Court for the State of Michigan

According to the lawsuit filed by Duggan et al., the group states it is their firm belief that a law requiring all drivers in the state to carry no-fault insurance coverage is in direct conflict with a Michigan Supreme Court Finding. This finding is the result of Shavers vs. Kelly in 1978, stating, ” a driver’s license, once issued, is a significant interest subject to constitutional due process protections.”

In the claim filed by Duggan et al. the complaint is that the high cost of no-fault insurance impedes due process for anyone with a Michigan driver’s license. Because the state requires all motorists to carry this type of coverage and pay its incredibly high cost, it stops many drivers from seeking employment or educational opportunities, going shopping for food and necessities, even taking their kids to school.

The Law was Supposed to Drive Insurance Rates Down

When the law first passed in 1973, the impetus behind it was to drive insurance rates down and ensure victims of auto accidents would receive compensation that was adequate and in a timelier manner. With this the new law, victims could no longer take the responsible party in an automobile accident to court. Instead, victims would be able to go to their own insurance companies for compensation. The impetus was to drive auto insurance premiums down and reduce the level of litigation, the exact opposite happened, and insurance premiums skyrocketed. In fact, the average cost of insurance nationwide is $1512.00 per year. In Michigan, the average price for auto insurance is $3,509.00. More specifically, motorists in the City of Detroit pay the highest auto insurance rates of any city in the country.

It Gets Worse (If That’s Possible)

If having outrageous insurance rates isn’t bad enough, the 1973 law has made criminals out of otherwise perfectly “honest ” citizens. In Michigan, approximately 20 percent of the cars on the road are running around uninsured. One of the highest rates in the country. In turn, the high number of uninsured motorists causes insurance rates to go up even further.

When the law passed, the Michigan Supreme Court stated that the No-Fault law is constitutional providing insurance rates were not unfairly discriminatory or excessive. This left a loophole that made the claim by Duggan et al. possible as rates have reached the point at which many have to choose between paying for insurance or buying food and paying the rest of their family bills.

Along with stating the law is unconstitutional, Duggan et al. ask that the state be given no more than six months to correct the law and take steps to reduce the high cost of insurance. If at the end of the six-month period a solution has not been found, the state should be required to return to the traditional tort system. While the outcome of this case may have a significant impact on future insurance rates, it does not help to find cheap car insurance right now under the current laws. What you need is an agency that will work with you to find the right insurance coverage based on your needs and budget.

Whether it is a fender-bender or major collision it is enough to leave you shaken, especially if there is damage to your property — or worse yet, injury to you. If you are going to report an accident to an insurance company, there is a process to help things go smoothly.

Do I report an accident?

Sometimes the most difficult part of making an insurance claim is deciding whether you even want to make one. There are times when it is more economical to take care of the damages on your own than to make a claim. There are two types of insurance claims that you can file: a first-party claim and a third-party claim.

When you file a first-party claim, you report the accident directly to your own insurance carrier. When making a third-party claim, you contact the insurance company of the other motorist involved in the accident. A third-party claim is made when the other driver was “at-fault.” If you are at fault and the damages to your car or the other car are minimal, it is best to consider how much it will increase your premiums to report the accident versus how much it would cost to fix the damages. If there are injuries involved or the accident was substantial, then it is always best to get the insurance company involved.

Report the car insurance claim

Although you may be a little shaken, it is important to report the accident immediately to the proper insurance carrier. If you are filing a first-party claim, then you will want to call your insurance carrier and should have their contact info either online or on the back of your insurance card. If you are filing a third-party claim, then you will have to get the information about the insurance company from the other motorist. Other things you will likely need when making a third party claim are:

The policy number

The insured person’s full name

The time and date of the accident

The license plate numbers for all parties involved

The police report number

A general description of the accident

The insurance company will be responsible for investigating your claim and arranging a time for you to have your car inspected for damages. They will typically have someone come out to assess the damage, unless the accident was severe enough that the car was totaled.

Each carrier will have their own timeline for filing a claim, which is why it is imperative that you call immediately to file.

What not to say when you call

There are certain questions that the insurance carrier is going to ask you. Because the call will be recorded, it is important that you not say anything that might jeopardize the case. There are many things that you will want not to talk about with the other insurance company, like:

Giving a report of your injury – Although you should tell them you are injured, do not give any more specifics about how you were injured or the extent of your injuries when you’re first filing a claim. Any statements about self-diagnosing can come back to bite you.

Submitting a written statement – Never give any written statements related to the accident unless you know exactly why you are providing them. And it is always a good idea to have Los Angeles auto accident lawyers look over any written statements before you send them.

Answer any specific questions – Avoid answering any specific questions about the accident. Don’t offer any conclusions of your own or give more details than are asked.

Tell the truth – It is imperative to tell the truth. Even if you are worried that it might put you at fault, if you are caught telling the insurance company something that isn’t true, that is technically fraud.

Agree to any settlements – Before you accept any settlement money, it is important to have your case assessed by a personal injury lawyer to ensure that you are being fairly compensated. Once you accept money then the case is over, and you aren’t eligible to collect for anything that may creep up in the future.

If you are in an accident where there is either damage or injuries, it is always best to get the help of a personal injury lawyer who specializes in auto accidents before you discuss any specifics of the case or agree to any settlements made by an insurance company.

The National Highway Traffic Safety Administration (NHTSA) recalled 51 million cars and trucks in 2015.

The NHTSA and car manufacturers issue car recalls when it is determined that there is a safety-related defect with a specific model. A car recall can also be issued if the car model does not comply with safety standards set by federal authorities.

When vehicles are recalled, an alert is issued to car owners. The car owner is then required to return the car to the dealership in order for the issue to be repaired. The repair is done at no charge to the vehicle owner. In extreme and rare cases, the entire vehicle may be replaced.

Photo Wikipedia

How Vehicle Recalls Affect Insurance Premiums

One of the many thoughts that go through a car owner’s mind when they receive a notice of a car recall is how it will affect their insurance premiums. The following are some things to keep in mind when faced with a vehicle recall.

Your insurance rates won’t be affected

Your insurance rates shouldn’t be affected by the recall. The insurance company is not responsible for the repairs, the manufacturer is. Your insurance company therefore will have no reason to raise your insurance rates especially if the safety issue is resolved. You will however need to provide proof of paperwork showing your insurance provider that the safety issue was repaired.

Ignoring a recall may cause insurance rates to rise

When you get a recall notice from your manufacturer, be sure to have the vehicle fixed at the dealership as soon as possible, even if it is a minor problem. Neglecting to get the vehicle repaired may result in an accident. Insurance providers will increase your rates if you ignore the recall notice.

Insurance rates are higher for cars with repeated recall history

If you’re shopping for a car, it’s a good idea to check the recall history of the model or manufacturer. If a certain vehicle’s make and model has been consistently recalled for safety issues, your Insurance provider could issue higher insurance rates as your vehicle has proven to be unreliable.

Not all recalls are the same

Some recalls are for small issues, such as a misplaced sticker, and can be fixed quickly. Other recalls are for major issues and could put your safety at risk. It is therefore important to have your car checked as soon as possible.

What to do When You Get a Vehicle Recall Notice

According to a study by J.D. Power, one in six cars on U.S. roadways are unrepaired despite an outstanding vehicle recall. This puts drivers and other road users in danger. When you receive a recall notice, make sure you:

Contact your dealership

Your car should be returned to the dealership for repair. Don’t take it to your local repair shop. The dealer will have the car repaired at no cost to you. Depending on the issue and the size of the recall, it may take a few minutes or a few months to have your vehicle repaired.

Contact your insurance provider

Provide your insurance agent with documentation showing that your vehicle has been repaired. This will show that you complied with the recall notice and that your vehicle is safe to drive. Your insurance provider will not increase your rates.

Beyond making sure that your vehicle is safe, it’s important to have insurance that you can depend on. Finally, auto insurance comparisons will help you find an auto insurer that will cover your needs at an affordable price.

You’re a smart and savvy consumer, always looking for a way to save money while still getting the best service. Because of this, you’ve probably done a lot of car insurance comparison shopping. It’s great to take charge, but the road to best and most affordable car insurance isn’t without pitfalls.

Below are some of the most common car insurance comparison mistakes and how to avoid them.

Mistake #1: Not Shopping Around

You have to start somewhere, and by far one of the biggest mistakes you can make is purchasing the first insurance package you come across. How can you possibly find the coverage that best suits your needs and budget if you don’t compare?

Mistake #2: Not Providing Accurate Information

When you’re using car insurance comparison sites like CoverHound, you are directed to fill out an online form. This form asks you several questions in order to gain information used to generate a quote. If you enter details that are incorrect about your car, or give inaccurate answers to questions about your driving record, you’re not helping yourself. If you have traffic violations or previous accidents on your driving record, your car insurance package will reflect it. The only way to get an accurate quote is to provide all the necessary and correct information to the best of your ability.

Mistake #3: Misunderstanding Coverage

If you don’t do your research before shopping around, you may fall into the trap of buying coverage you don’t really need—or worse—not buying enough! Understanding the type of car insurance your state requires motorists to carry is essential to finding a package that works for you. This is a big help when comparison-shopping for auto insurance, because if you know precisely what your needs are, you can whittle down the competition and find an insurance package you need at a price you can afford.

Mistake #4: Failing to Consider the Extras

You may think that you only need to buy the minimum amount of insurance required by your state, hoping to save money by not getting the extra add-ons insurance companies provide. For example, you may have coverage to repair your vehicle if an accident should occur, but what will you drive in the meantime? Unless you have an extra car, you should consider whether or not you need a policy that will cover a rental car while yours is in the shop.

A good strategy is to familiarize yourself with the ins and outs of any car insurance policy you’re thinking of buying while weighing the extra add-ons that may come in handy.

Mistake #5: Concentrating on Cost Alone

One of the misconceptions about shopping for car insurance revolves around the idea that the less money you pay, the better the deal. What you really should be looking at is what you’re getting for the price of the policy. Make sure you examine all of the things included in the policy; this is the only way to truly compare different policies. Just because a company offers a good deal on minimum coverage doesn’t mean that they’ll offer a better deal on higher coverage policies.

In the End

When you finally make the choice toward an insurance plan, you want to rest easy knowing you’re not only getting your money’s worth, but also the coverage you need in case of an accident. Use the knowledge you’ve gained here to go out and get the right coverage for the right price!

Today, we’re going to talk about a crucial part of your personal finances; insurance. More specifically, we’re looking at four types of insurance you need to have:

This is perhaps the most well-known and talked about insurance. If you ask someone to name an insurance type, the majority will say car insurance. But, what is it and why do you need it? Basically, it insures your car against different kinds of damage. This means that if you get into an accident, your insurance provider will pay for any repairs that are needed. Obviously, this can save you a lot of money, and I mean a lot. If your car is severely damaged, you can get it fixed through your provider and save tonnes of money. Without insurance, you might have had to fork out lots of money on a new car. Plus, it’s illegal to drive a motor vehicle without it being insured. So, you have to make sure you’ve got it for your car. There are tonnes of providers out there that will give you quotes depending on a few factors. Age, gender, driving experience, and the car you drive can all have a bearing.

Home Insurance

Another type of insurance that you must have is all to do with your home. Yes, home insurance is essential for anyone that owns property. With it, you’ll get the option to protect two aspects of your house. You can get accidental damage cover and contents cover. The first of which will protect you if your home gets damaged for whatever reason. Maybe a storm damaged your roof, or someone broke your window. Either way, if your home insurance covers this, you’ll have the repairs paid for. Contents cover will protect you if your house ever gets burgled. If someone steals items from your house, you’ll be covered. Similarly, home insurances will protect your possessions if they get damaged in floods, etc. Some companies will give you replacement items free of charge. If you own a property, then you can’t forget about home insurance, trust me.

Life Insurance

Life insurance is something that no one likes to think about, but it’s very important. You see, we get life insurance to cover our family in case we die. As you can tell, this is a very sensitive topic, which is why people don’t like thinking about it. No one wants to talk about death, but sometimes you have to. With life insurance, your family will get money paid to them, if you pass away. This means they’re going to be financially stable when you’re gone. You may be the primary money maker in your house, so if you’re not there to earn money, they could be in trouble. Thankfully, life insurance ensures that your family finances are not ruined by your death. Types of life insurance can vary, some come with critical illness cover, others have certain requirements. Although you don’t like to think about it, death is inevitable. It makes sense to give your family some financial gain when you pass away.

One of the most important things in life is your health. If you aren’t healthy, you need to get treatment and see a doctor. Doctors can help you get better and back to feeling your best. When you have health insurance, seeing medical professions is a lot easier. In fact, some institutions only accept people that have insurance. What health insurance does is protect your health and wellbeing. It can cover the cost of doctors appointments, operations, physical therapy, etc. Without it, it’s very hard to find reliable, high level, medical care. Sure, there are some public options for people without insurance. However, the waiting times for appointments are insane, let alone the wait for surgeries. Without health insurance, you could be waiting for surgery for up to two years! But, if you have it, you can get the surgery covered by your insurer and make sure you’re seen to as soon as possible. It’s highly recommended for everyone, particularly those with a family.

Insurance is a very important part of your financial life. It can protect you from so many things and ensure you aren’t paying loads of money for different stuff. Imagine if you had none of the insurance above. Think about how much money you’d have to pay to cover things like car breakdowns, medical bills, and so on. Getting insurance can give you a more stable life, and set your family up for a comfortable future.

As summer draws to a close, local municipalities across the country are gearing up for the winter months ahead. When the weather gets harsh, the biggest concern will be road safety. Freezing conditions and snow will wreak havoc on America’s roadways, and local crews will work around the clock to ensure safe passageways for all motorists.

In particularly downtrodden cities like Detroit and Cleveland, fluctuating temperatures, snow, and ice will contribute to a problem that continues to grow year by year, placing major stress on local budgets – potholes.

Last spring, “unprecedented wear and tear” had cities exhausting their budgets in order to fix potholes, such as New York City, which filled more than twice as many potholes in the spring of 2014 as it did the previous season. It is feared that many roads will be even worse off after we get through this winter. With many areas lacking the funds necessary to fill all their potholes, individuals drivers must be extra cautious to avoid damage to their vehicles.

Here are some tips you can follow to deal with potholes while traveling and to minimize any potential damage to your car and tires:

Increase the distance between your car and those in front of you. You’ll have extra time and space to deal with unexpected dips and craters in the road.

Be aware of traffic patterns. If you notice other drivers swerving ahead, you’ll be clued in to a potential pothole coming up.

Watch the road. Be sure to look at the roadway while driving so that you can spot any upcoming potholes or other obstacles.

Slow down. Drive very slowly through potholes to minimize potential damage to your car. It is better to roll through a pothole than to stop suddenly.

Avoid swerving as a reaction to sudden potholes. Turning into oncoming traffic or hitting pedestrians/bicyclists is much more dangerous than going through a pothole.

Keep your tires properly inflated. Over-inflated or under-inflated tires are much more susceptible to damage from driving through potholes.

Regularly check your tires for blisters, and use the “penny test” to make sure your tire treads aren’t worn down too much. Also be on the lookout for any changes to your car’s alignment.

If you drive through a bad pothole, immediately check your tire and hubcaps for damage. If there is any, get it fixed as soon as possible so it doesn’t get worse.

File a timely claim with your car insurance company if necessary.

Change your driving route whenever possible to avoid major potholes until they can be fixed.

Because potholes are dangerous, local transportation authorities do take them seriously. Unfortunately, many budgets are stretched so thin that potholes, especially smaller ones, may not be fixed for long periods of time. Winter weather often causes potholes to appear and get bigger, so most municipalities use suppliers like Mchlaughlin Underground, that supply large vacuum excavation machines, until the springtime, when most of the risk for additional road damage has passed.

If you notice a pothole in the road, you can contact your state transportation department to report it. You’ll need to provide the exact location of the pothole (intersection, lane, nearby landmarks, etc.), and it’s helpful if you can provide information about its size (approximate length, width, and depth), as well as noting if there is any reason for particular concern (interference with a bus stop, trolley track, or pedestrian crosswalk, for example).

Britain’s used car market is more than four times larger than the new car market – almost 9 million people every year purchase a second-hand car. What Car? with the assistance of other used car industry experts, has picked the best used cars for sale in 2013.Vauxhall received several individual car awards and the brand also won the title of Best Used Car Manufacturer of the Year, thanks to its long-running Network Q used car scheme. Steve Huntingford, What Car?’s road test editor and head judge, said:

“Although Network Q is one of the oldest approved used schemes, there are more than 350 outlets and it has a good online offering, a great choice of stock, all cars come with a comprehensive Network Q check, and an unbeatable insurance package. Network Q makes buying a used car very easy.”

Volkswagen Golf 1.4 TSI SE 5dr was named Used Car of the Year 2013. You can find this car at a dealer price of approx £8,700 and a private price of around £8,300. What Car? praised the Golf’s impressive cabin quality and refinement, comfort, running costs and impressive safety credentials. The Golf’s win corresponds with data taken from the AA’s website, which shows that twice as many people viewed a Volkswagen Golf than any other used car in the last 12 months and one in 26 views of cars on their website were of a Golf model.

“The Golf is the true ‘car of the people’ as it is practical, economical, sporty, safe, desirable, reliable and fun. Twice as many people viewed VW Golfs on AA Cars in the last year than any other car.”, Edmund King, AA president for The Telegraph

“What clearly sets the Golf apart from other small family cars is its cabin.”

Other awards won were:

Best used small car 2013: Vauxhall Corsa 1.2 Design AC 5dr

Age/reg: 07/07

Dealer price/private price: £4,100/£3,600

Best used family car 2013: Volkswagen Golf 1.4 TSI SE 5dr

Age/reg: 10/10

Dealer price/private price: £8,700/£8,300

Best used estate car 2013: Mazda 6 Estate 2.2D 163 TS2

Age/reg: 09/09

Dealer price/private price: £11,400/£10,700

Best used MPV 2013: Ford S-Max 2.0 TDCi Zetec

Age/reg: 09/09

Dealer price/private price: £10,900/£10,000

Best used SUV 2013: Nissan Qashqai 1.5 dCi Acenta

Age/reg: 07/07

Dealer price/private price: £7,800/£7,200

Best used executive and luxury car 2013: BMW 320d SE

Age/reg: 07/57

Dealer price/private price: £9,000/£8,600

Best used fun car 2013: Renaultsport Clio 200 Cup

Age/reg: 09/09

Dealer price/private price: £7,500/£7,200

Best nearly new car 2013: Vauxhall Astra 1.6 Exclusiv

Age/reg: 12/12

Dealer price/private price: £9,100/£8,700

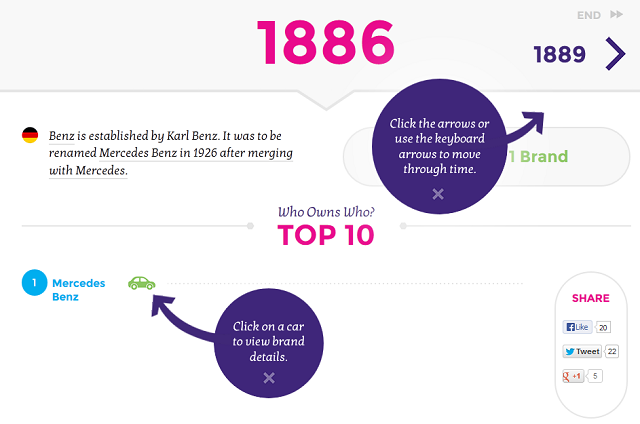

A History of Car Manufacturers

Car manufacturers jumped into car production in the late 1800’s with the pioneers of the industry being Benz, Peugeot and Daimler followed by Fiat, Opel and Renault. MoneySuperMarket created a a visually appealing and easy to follow info graphic called A History of Car Manufacturers that shows the way the car manufacturing industry evolved and changed over time. It’s interesting to know how the auto industry got from one manufacturer in 1886 to 42 parents and 90 brands over a period of 125 years. Be sure to let us know if you’re one of the 99% of Britons that saved on the cost of their car insurance when they used MoneySuperMarket.

Insurance companies tend to apply greater prices on the car insurance policies for low-income people, a study published by the Consumer Federation of America shows.

“Lower-Income Households and the Auto Insurance Marketplace: Challenges and Opportunities” is the report wrote by Stephen Brobeck and J. Robert Hunter. They reviewed the literature from academics and regulators and added new findings from their research.

The cost of car insurance can be a heavier burden than the cost of the car, in certain cases. And this leads to economic implications, the authors say.

“There is much academic research that clearly shows that if you have ready access to a car, it dramatically improves your economic opportunities. The release of the report is just the beginning of our initiative to try to inform the country, particularly state regulators, who can do a great deal to mitigate the problems,” said Stephen Brobeck, executive director at the Consumer Federation of America.

The legislation prevents insurance companies to establish premiums on income base, but they have the possibility to take in consideration the driver’s education, occupation, home address, and credit rating.

According to the Consumer Federation of America, these data can replace the information on income and until now there were no studies on what impact has this combination of factors on the poor persons.

“We think education, occupation and credit scores are surrogates for income. Occupations that have no driving risk affiliated with them but do have lower incomes tend to pay more, so it raises serious questions,” said J. Robert Hunter, director of insurance at the group.

“In some areas, many responsible lower-income drivers are required to spend more than $1,000 a year for liability coverage that is often unfairly priced and provides no real insurance protection to them,” said Stephen Brobeck.

Around 14% of the car owners drive without insurance, according to an estimation made by the Insurance Research Council in 2007. In people with low or moderate income the rate is probably double, said J. Robert Hunter.

Car insurance premiums tend to be more expensive for poor people.

Car insurance cost represents a big part taken from the income for low-income workers, who regularly need to drive to work. As a consequence around 20% of car owners who earn $37,000 or less annually do not have car insurance, the authors say.

Generally homeowners pay less than persons who do not own their homes. People with low education, with less skilled occupations also have to pay more. For them premiums are 40% higher, according to a 2006 study cited in the report. The prices also rise when it comes to drivers with a flawed or a thin credit history, or to persons who had a coverage with lower limits on bodily injury.

The price of the insurance policy generally reflects the price of the car, but even a very used car, a jalopy can cost $700 to $1,000 per year, says the report. The median national cost is $835, but it weighs a lot for poor people.

The study also found that some insurers were charging more for policies with less coverage, which, they said, is likely to disproportionately affect lower-income households since they may be more likely to buy those policies.

“Some companies charge more for the basic limits for the state than they would for higher limits for the exact same driver. It’s like going into a store and saying, ‘I want a box of cereal,’ and the big box is much cheaper than the little box,” J. Robert Hunter said.

This kind of tendency also hurts poor people because they are more likely to buy the minimum coverage policies.

With only one exception, New Hampshire, car insurance is mandatory across the United States.

“The big problem is that mandatory coverage is so expensive, often costing over $1,000 in urban areas that it prevents them from buying a car,” said Stephen Brobeck.

The states have to ameliorate the access to low-cost car insurance, since California is the only state with a strong low-rate coverage program, the report says.

“The states are cracking down on the uninsured. If they are going to do that, they have a responsibility to ensure that lower income people can afford to drive,” said Stephen Brobeck.

The number of miles driven is considered a factor that diminishes the risk of accidents and it may reduce premiums, but it has an improper importance in the insurance industry’s classification system, says the report.

“Poor people, we know from the data, they spend a lot less on gas, which means they are driving less. So if insurers more fully reflected miles driven in pricing, it would lower the rate for poorer people,” said J. Robert Hunter.

In California, drivers who own a vehicle worth less than $20,000 and who have incomes of less than $27,000 to $55,000 (depending on family size) and who have driven at least three years with a clean record can qualify for minimal liability coverage at relatively low rates.

The annual premium for drivers in the program was $358, the report says. This also happens to be the highest premium the program charges in all of California. The average annual premium in Los Angeles was $802.

Also lowering the minimum amount of liability insurance that lower-income households are required to purchase was proposed by the authors.

J. Robert Hunter suggested to the Federal Insurance Office to collect more data regarding the car insurance cost for low-income persons.

This website has updated its privacy policy in compliance with EU GDPR 2016/679. Please read this to review the updates about which personal data we collect on our site. By continuing to use this site, you are agreeing to our updated policy. AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.